THE BIG SHORT TO BHARAT: DECODING CREDIT DEFAULT SWAPS AND INDIA'S MISSED OPPORTUNITY

- Pranay Bedi Verma, Akshay Grewal, Ananya Mehta

- Jul 31, 2025

- 6 min read

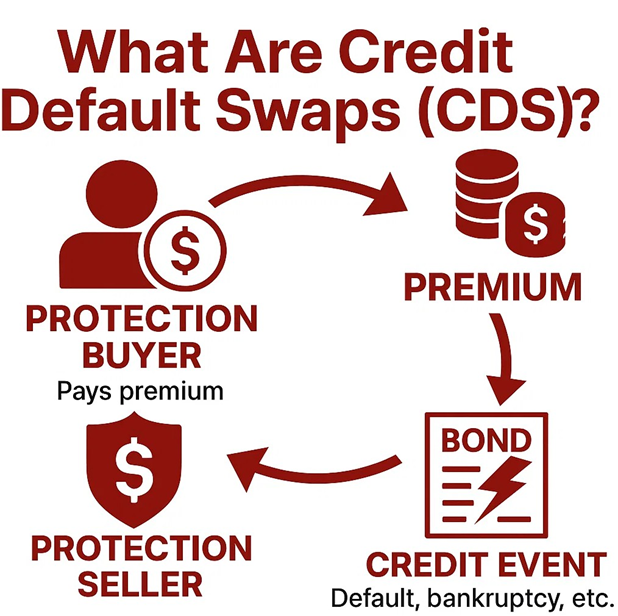

Introduction: What Are Credit Default Swaps (CDS)? A Credit Default Swap (CDS) is an over-the-counter (OTC) financial derivative contract where one party (the protection buyer) pays a periodic premium to another party (the protection seller) in exchange for protection against a credit event, such as default, bankruptcy, or failure to pay on debt instruments (e.g., a bond or loan). Basically, it is like insurance against the default of a borrower.

CDX (Credit Default Swap Index): A CDX is a tradable index comprising a basket of CDS contracts on multiple entities (e.g., corporations or sovereigns). It allows investors to gain exposure to or hedge against the credit risk of a group of issuers.

Breaking Down CDS: Key Terms and Concepts

Firstly, let’s dive into how premium calculation is central to the contract. The CDS premium, or spread, is the periodic payment made by the buyer to the seller. It is quoted in basis points per annum of the notional amount. It reflects the market’s sentiment about the credit risk. The higher the risk, the higher the premium

The credit spread is used to price CDS. It represents the difference in yield between a corporate bond and a risk-free government bond. A wide credit spread indicates deteriorating credit quality and increased default risk which increases the cost of the CDS.

The notional value is the face value of debt that is protected by CDS. It determines the maximum payout the seller would be liable for if a credit event occurs.

Maturity refers to the duration of the CDS contract. It often ranges from one to ten years. The contract remains active either until maturity or when a credit event triggers settlement. Maturity influences the contract's pricing as longer tenures lead to greater uncertainty and risk.

Why Use CDS? Hedging, Speculation, and Market Signals

Hedging is the most straightforward use. Investors holding bonds can purchase CDS to safeguard against losses from credit events.

Speculation allows investors to profit from anticipated changes in credit quality without owning the underlying bond.

Lastly, CDS spreads provide market signals. They reflect investor sentiment about credit risk. They are swift to change.

Case Studies: When CDS Changed the Game

1) The $27M Pandemic Hedge: Ackman’s 100x CDS Bet Against Corporate Credit

Back in March of 2020, when the Markets Braced for the impact of COVID-19, A billionaire investor, Bill Ackman, placed a $27 Million Hedge, which earned him over $2.6 billion in returns over 30 days.

Background:

William Albert Ackman, famously known as Bill Ackman, is an American Billionaire, Hedge Fund Manager. He is the founder and CEO of Pershing Square Capital Management, a hedge fund, $15 billion in assets under management.

2015 - 2019: Bill’s Fund shrank by about $9 billion, due to risky bets; however, the fund bounced back in 2019, generating a commendable 58.1% return

Early 2020: The fund was highly concentrated in the following sectors

Ackman Foresaw the COVID effect and made a brilliant trade using CDX ( Credit Default Swap Index)

The Strategy:

03/03/2020: Bill issued a statement to his investors, highlighting concerns over downward volatility in the Market following the upsurge of COVID. He also mentioned something about purchasing a notional hedge with asymmetrical payoffs, basically a low-risk, high-reward Hedge, which we now know are CDX

The Trade:

Early March: Bill bought CDX for a notional value of $65 billion( value of corporate bonds), the credit spread ( Difference between bond yield of corporate and government bonds) was 0.5%, showing a high trust in the corporate bonds not failing. The Annual Premium for these CDX would be $65 Billion X 0.5%, i.e. $325 million, or $27 million per month.

The basic reasoning behind this move was that as investor confidence shook due to COVID, and credit default would rise, so would the price of his CDX; it was basically a bet in favour of corporate bankruptcy. And so it paid off!

23/03/2020: Bill issued a statement that they completed the exit of these CDX for $2.6 billion dollars, by paying only a month's premium, i.e. $27 million per month

How was it Worth so much? In the few weeks that followed, Credit spreads rose to 1.4% from 0.5%, meaning if someone wanted to protect the same corporate bonds worth $65 billion, they would have to pay a premium of $910 million a year, or $76 million a year

This meant, the value of his contracts now is the present discounted value of $ 76 M - $27 M, i.e. $49M per month, discounted for the remainder of the period, i.e 4 years and 11 months, which turns out to be $2.7 billion

2) The $1.3B Subprime Short: How CDS Made Michael Burry a Crisis Prophet

Background:

While Wall Street bet on the housing boom, one man was quietly preparing for its collapse. Michael Burry saw disaster where others saw endless profit. In the early 2000s, U.S. housing prices were soaring largely due to subprime mortgages. Big banks bundled these toxic loans into complex securities pretending that the market would never crash.

The man himself:

Burry, the founder of Scion Capital, analyzed mortgage data and realized many borrowers couldn't afford their loans. He used credit default swaps (CDS) to bet against subprime mortgage-backed securities. He basically bought insurance on a house he didn’t own, expecting it to burn down. When the housing market imploded in 2007–2008, Burry’s CDS positions exploded in value. In just a few months, he made over $700 million for his investors and $100 million for himself.

Aftermath:

After the crash, Burry shut down Scion Capital, returned money to investors, and shifted focus to personal investing. He later launched Scion Asset Management to pursue undervalued assets. Burry’s move proved that a single investor, armed with data and conviction, could expose systemic flaws. His strategy not only challenged Wall Street's strategies, it revealed how fragile the global financial system really was.

CDS in India: Policy, Progress, and the Roadblocks

Credit Default Swaps were once considered a niche in International Markets, but have become mainstream in the USA and European markets. But, I can’t say the same for Indian Markets. Despite some policy efforts and traction, CDS remain largely dormant and highly regulated

Policy Timeline:

2011: The RBI introduced CDS in Indian Markets for Corporate Bonds for the sole purpose of hedging. Participation was highly regulated, limited to only regulated institutional investors. The Purpose was to deepen the corporate bonds market and allow credit risk transfer

2013: RBI and SEBI finally acknowledged the limited interest and excessive regulations, due to which CDS didn’t gain traction. Possibly due to the largely illiquid bond market in India

2016: SEBI consults on expanding the use of CDS, considering expanding the scope to Mutual Funds and FPIs, however, no major reforms were implemented.

2022: This was a breakthrough year as the RBI released revised CDS guidelines. Participation broadened to Mutual Funds, Insurance Companies and FPIs. Cash-settlement was introduced, and unhedged-particiaption was finally allowed for certain market-makers.CDS were also permitted on AA and below-rated corporate bonds

2024: The Finance Ministry publishes a “White Paper” on the Indian economy, directly criticising CDS as a missed opportunity for Indian Financial Markets. Recommends, creating a centralised clearing system(Like in the USA) for CDS, integrating them with digital bond platforms and expanding to NBFC and SME credit markets.

2024: Opposition publishes a “Black Paper” as a counter-report, criticising that CDS exist only on paper, with no real market formation, and the lack of a centralised clearing system. Highlighting 0 CDS trading activity despite the 2022 reforms.Calls the White Paper, Aspirational, without institutional delivery.

Conclusion

The CDS market in India remains highly illiquid and underutilised. However, recent support by the government could pave the way to a developed CDS Market like the one in USA

Feature | India | United States |

Market Size | <$1 Billion Notional | $4 trillion Notional |

Use Cases | Hedging | Hedging, Arbitrage & Speculation |

Clearing System | None | Centralised |

Conclusion: CDS — Powerful Yet Underused in Emerging Markets

From Burry's billion-dollar vision to Ackman's pandemic bonanza, CDS have been revolutionary worldwide. India's experience is still in its infancy—hampered by regulation, infrastructure deficiencies, and policy complacency. But with increased government attention and institutional reforms, CDS can become an underappreciated tool rather than a foundation stone of India's evolving credit and debt markets.

Pranay Bedi Varma is an Analyst at IFSA Hansraj

Akshay Grewal is an Analyst at IFSA Hansraj

Ananya Mehta is an Analyst at IFSA Hansraj

References:

Burry, M. (2010, April 3). I saw the crisis coming. Why didn’t the Fed? The New York Times. https://archive.nytimes.com/www.nytimes.com/2010/04/04/opinion/04burry.html

Investopedia. (2021, March 12). 'The Big Short' movie explained. https://www.investopedia.com/articles/investing/021616/big-short-movie-explained.asp

Investopedia. (2024, September 3). Who is Michael Burry? https://www.investopedia.com/michael-burry-4683837

Bank for International Settlements. (2020). Credit default swaps: Mechanics and market developments. https://www.bis.org

Jarrow, R. A., & Turnbull, S. M. (1995). Pricing derivatives on financial securities subject to credit risk. The Journal of Finance, 50(1), 53–85. https://doi.org/10.1111/j.1540-6261.1995.tb05167.x

Reserve Bank of India. (2011). Guidelines on credit default swaps for corporate bonds. https://www.rbi.org.in

Pershing Square Capital Management. (2020, March 23). Investor statement on CDX hedge exit. Pershing Square Capital Management. https://pershingsquareholdings.com/wp-content/uploads/2020/03/Pershing-Square-Capital-Man agement-L.P.-Releases-Letter-to-Investors-March-26-2020.pdf

Reserve Bank of India. (2011). Guidelines on credit default swaps for corporate bonds. Reserve Bank of India. https://rbidocs.rbi.org.in/rdocs/content/PDFs/FGCD240511A.pdf

Reserve Bank of India. (2022). Revised guidelines on credit default swaps. Reserve Bank of India. https://rbi.org.in/scripts/NotificationUser.aspx?Id=12226

Comments